Composite Deck Monthly Payment by Project Size

Below are typical monthly payment scenarios for composite deck projects in Loudoun, Fairfax, Prince William, Arlington, and Alexandria. Figures use a sample 8.99% APR — slide the deck payment estimator for your specific APR and term.

| Project Amount | Typical Use Case | 10-Year /mo | 15-Year /mo | Total Interest (10y) |

|---|---|---|---|---|

| $15,000 | Composite resurfacing on existing frame | $190 | $152 | $7,800 |

| $22,000 | 250 sqft composite deck, mid tier | $278 | $223 | $11,360 |

| $30,000 | 350 sqft composite, mid tier, railings | $380 | $304 | $15,600 |

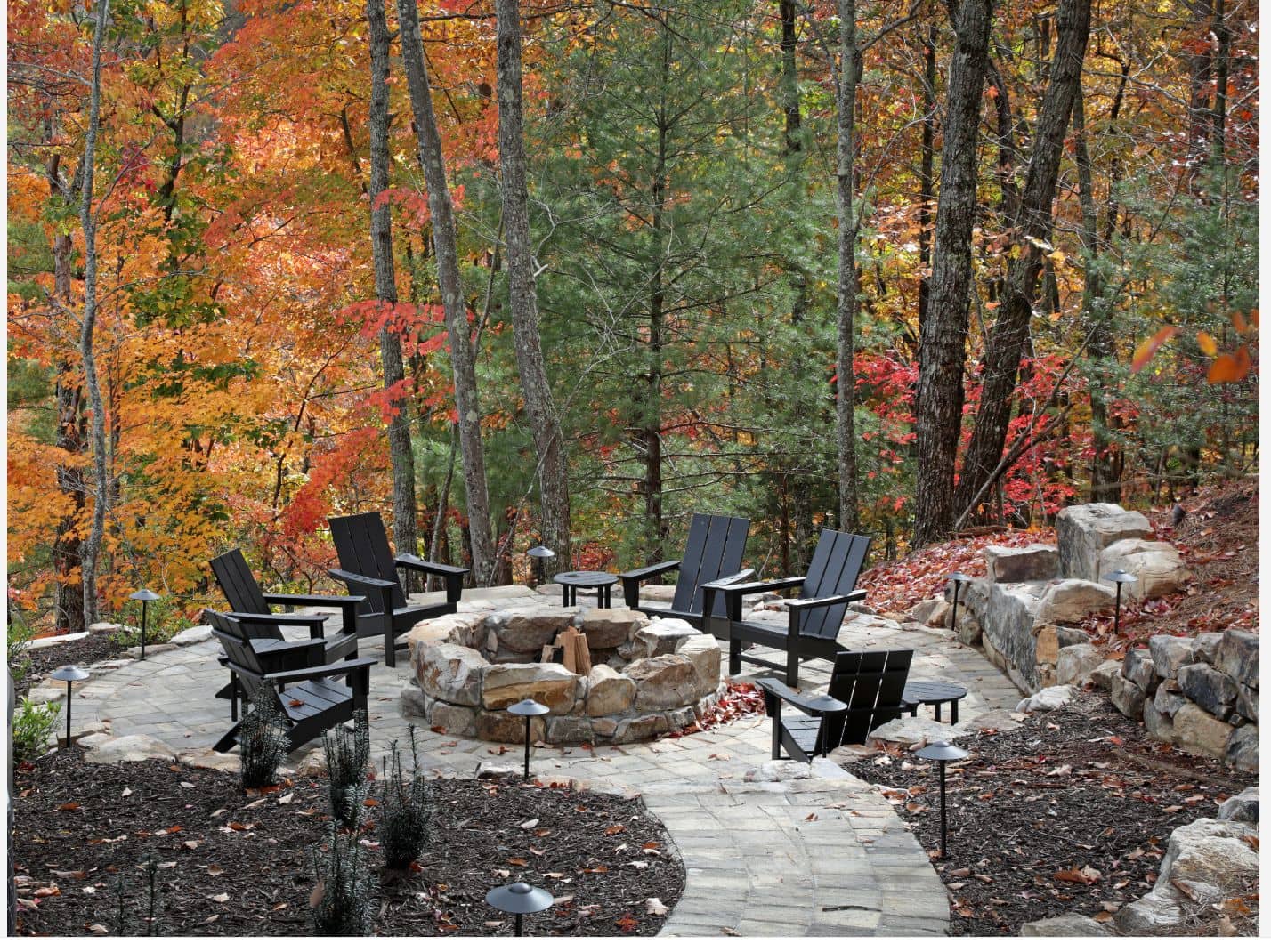

| $40,000 | 450 sqft composite, premium tier | $506 | $406 | $20,720 |

| $55,000 | 600 sqft composite + lighting + stairs | $696 | $558 | $28,520 |

| $70,000 | Covered composite deck w/ premium railings | $886 | $709 | $36,320 |

At 8.99% APR over 10 years, a $30,000 composite deck costs approximately $45,600 total — $15,600 in interest over the life of the loan. A 15-year term lowers the monthly payment to $304 but raises total interest to roughly $24,720.

Illustrative only at a sample 8.99% APR. The longer term lowers the monthly payment but raises total interest. Actual rate, term, and monthly payment are determined by your lender.

What Drives the Monthly Payment Up or Down

Three variables move the monthly number: project amount, APR, and term. APR is set by the lender based on your credit profile. Term is your choice — most home-improvement loans run 5, 10, or 15 years. Project amount is the part you control by scoping the deck correctly. For accurate pricing per material tier, see our composite deck cost guide for Northern Virginia.

What the Project Amount Should Include

The biggest source of error in a monthly payment estimate is a project amount that only covers the deck boards. The number you put into the calculator should reflect a complete written estimate:

- Composite or PVC decking material (Trex, TimberTech, Fiberon)

- Framing — either reuse on a sound frame or new pressure-treated lumber

- Hidden fasteners and joist tape

- Railings (composite, aluminum, or cable) and stairs

- Lighting (post-cap, riser, recessed deck lights)

- Demolition and haul-away of the old deck

- Permits for your county (Loudoun, Fairfax, Prince William, Arlington, Alexandria)

- HOA submission package and revisions

- Project management, design, and final cleanup

Composite vs Wood: Long-Term Cost Matters More Than Monthly

A composite deck typically costs 20–40% more upfront than pressure-treated wood, which raises the monthly payment slightly. Over 15 years the math reverses: composite avoids the $8,000–$15,000+ in cumulative stain, seal, sand, and board replacement cost that pressure-treated wood requires. The composite vs wood comparison covers 15-year total cost in detail.

Soft-Pull Pre-Qualification (No Credit Impact)

The estimator on this site is a model — your real rate and term come from a lender pre-qualification. We work with Enhancify, which returns multiple lender offers in roughly 60 seconds using a soft credit pull that does not affect your credit score. See the full process on our deck financing page.

How Northern Virginia Homeowners Typically Plan a Financed Deck

- Use the estimator to find a monthly payment that fits the household budget.

- Request a free on-site visit and a written, itemized project estimate.

- Pre-qualify through Enhancify (soft credit pull) to confirm the real APR and term.

- Compare offers — many homeowners pick the offer with the lowest total interest, not the lowest /mo.

- Sign the contract and start the permit + HOA process while financing closes.

- Build begins; final invoice is paid by the lender directly when the deck is complete.

FAQ

How much is the monthly payment on a $30,000 composite deck?

At a sample 8.99% APR, a $30,000 composite deck financed over 10 years is roughly $380/month and roughly $304/month over 15 years. The longer term lowers the monthly payment but raises total interest. Your real rate and term come from a lender pre-qualification, not from the estimator.

What APR should I model for deck financing in Northern Virginia?

Most home-improvement financing in Northern Virginia for credit scores in the 680–740 range models in the 8–11% APR band. Promotional 0% interest options exist for shorter payoff windows. Pre-qualification through a soft credit check returns the real number without affecting your credit score.

Can I use home equity instead of unsecured deck financing?

Yes. Home equity loans and HELOCs typically carry lower APRs than unsecured home-improvement loans, but they take longer to close and put the home as collateral. Many Northern Virginia homeowners use unsecured financing for speed (project starts in days, not weeks), then refinance later if needed.

Does the monthly payment include permits, HOA, and railings?

It should. The project amount you enter into the estimator should reflect the full written estimate — decking material, framing reuse or replacement, railings, stairs, lighting, demolition, permits, and HOA submission. Modeling only the deck boards understates the real monthly payment.

How quickly can a financed composite deck project start?

Pre-qualification through a soft credit check usually returns offers in 60 seconds. Once a lender is selected and the loan funds, the construction timeline is the same as a cash project — typically 4–8 weeks from contract to finished deck, including permit review and HOA approval.

Does financing add cost vs paying cash?

Yes. Financing adds interest cost over the life of the loan. The trade-off is keeping cash reserves intact and building the deck during the right season. Many homeowners model both: total interest over the term vs the opportunity cost of paying cash upfront.

Will checking my financing options affect my credit?

Pre-qualification uses a soft credit pull and does not affect your credit score. A hard inquiry only happens if you choose a specific lender offer and move forward with a full application. The estimator on this site does not check credit at all.

Model Your Real Monthly Payment

Move three sliders — project amount, APR, term — and the estimator returns your monthly payment in seconds.

Open the Deck Payment Estimator →